In December 2024, we carried out in-depth research into the use of artificial intelligence and data analytics within credit risk management processes at financial institutions.

The research was based upon data analysed for the period 1st January 2023 to 1st November 2024. The content we reviewed included intelligence on technology procurement, technology releases, vendor partnerships, vendor corporate activity, and other industry developments.

This article aims to provide an easily digestible summary of some key outcomes from this research.

Alongside this ‘use case’ focused research, we will shortly issue a follow up Vendor Spotlight Report which will be specifically organised around the leading software vendors within this field. Keep an eye out for this report and associated blog article coming soon.

The full research is available for subscribers to download on our website.

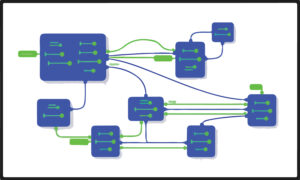

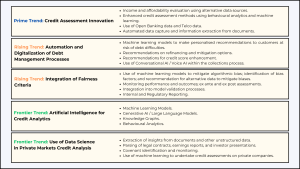

The diagram below provides a summary view of the themes and trends identified within this research.

Strategic Overview and Key Takeaways

The Landscape Continues to Rapidly Evolve

There is a wide maturity range in the overall scope of applications of artificial intelligence to credit risk management in financial institutions.

- Some of the themes identified are now verging on mainstream usage. A particularly material development is observable in the use of AI to expand access to credit for demographic groups which traditionally have been ‘underbanked’ or have a ‘thin credit file’.

- Expanding income and affordability assessments to leverage alternative data sources and use behavioural modelling techniques is a significant development in this field.

- We see this trend globally with insights identified in diverse locations including Brazil, Canada, Mexico, the United Kingdom, the United States, and a particularly notable amount of activity in The Philippines.

- In many areas there continues to be a large amount of innovation and experimentation, much of which is being led by market software and solution vendors. We are currently tracking over 30 vendors with AI driven solutions for credit risk management, with many more emerging on the horizon.

- New funding of AI driven credit risk vendors in the past 2 years suggests this market will continue to develop. Examples of vendors receiving new funding over this period include: Accelex, AI, Alphastream, Clerkie, CrediLinq.Ai, Credit Genie, Credora, EnFi, Finexos, KlariVis, martini.ai, Nova Credit, Okredo, Otto, Prism Data, Stratyfy,.

Benefits are Not Purely a Function of Size or Scale

Advancements are not simply a function of organizational size. Innovation is also being driven by institutional agility and pain points.

- For many use cases, it is smaller institutions such as credit unions, community banks and fintechs which are leading the experimentation in partnership with market solution vendors.

- That being said, the use of AI for credit risk within global and regional financial institutions is rapidly progressing. In this report, we have highlighted Annual Report references on this topic from a diverse group of international financial institutions including: American Express, Bank of China, China CITIC Bank, China Guangfa Bank, CIMB, Development Bank of Singapore, Discover, Hana Financial Group, HSBC, ICICI Bank, Itau Unibanco, JP Morgan, Kasikornbank, Siam Commercial Bank and Toronto Dominion.

Early Adoption is Driven by Data Availability

In general, the use of AI is most developed within credit risk management processes for Consumer Banking and SME / Commercial Banking in comparison to larger scale Corporate Banking. This is perhaps understandable due to the greater availability of data when the volumes of customers are larger.

- We do, however, see evolving developments and experimentation in the application of AI to the larger ticket and more structured needs of both Corporate Banking and Private Markets Investment Credit.

- More broadly, we expect all segments of the credit risk value chain to see an increased use of these innovative techniques once the technological foundations are embedded.

Building the Foundational Components will Serve a Broad Range of Use Cases

Many of the highlighted themes have significant overlap. Examples being:

- Innovation in credit assessment leans heavily on use of new analytical modelling techniques.

- Expanded use of AI models within credit assessment then requires investment into new solutions and capabilities to ensure fairness criteria are considered and respected.

- Many of the solutions leverage a similar set of core technological features (and associated people skills) such as innovations in document extraction, intelligent process automation, orchestration through agentic methods, and machine learning modelling. This will likely mean, therefore, that a bank successfully deploying for one use case may then more easily deploy these same capabilities to further use cases (in both credit risk and beyond) with only marginal incremental investment required.